Labelling savings as environmentally friendly is a marketing ploy that needs a policy approach, writes Pietro Moro.

Honolulu (Brussels Morning) Securities labelled as “Environment, Social, Governance” (ESG) are a fast-growing market with double-digit expansion. The market is one step ahead of the regulators and there is clearly a need to catch up, to avoid “green-washing”.

“Green washing” is about branding investment in specific securities and funds as “environmentally friendly”, promising to turn your savings into a force for good. Often, the promise is idle or just an added layer of marketing to an asset that has little to do with reality, according to the GIIN Annual Impact Investor Survey 2020.

This mislabeling represents a structural risk to the market, which, if left unaddressed, will leave investors who look to drink real pure juice faced with downing a mug-full of sugary Kool-Aid.

Fast-growing juice stand

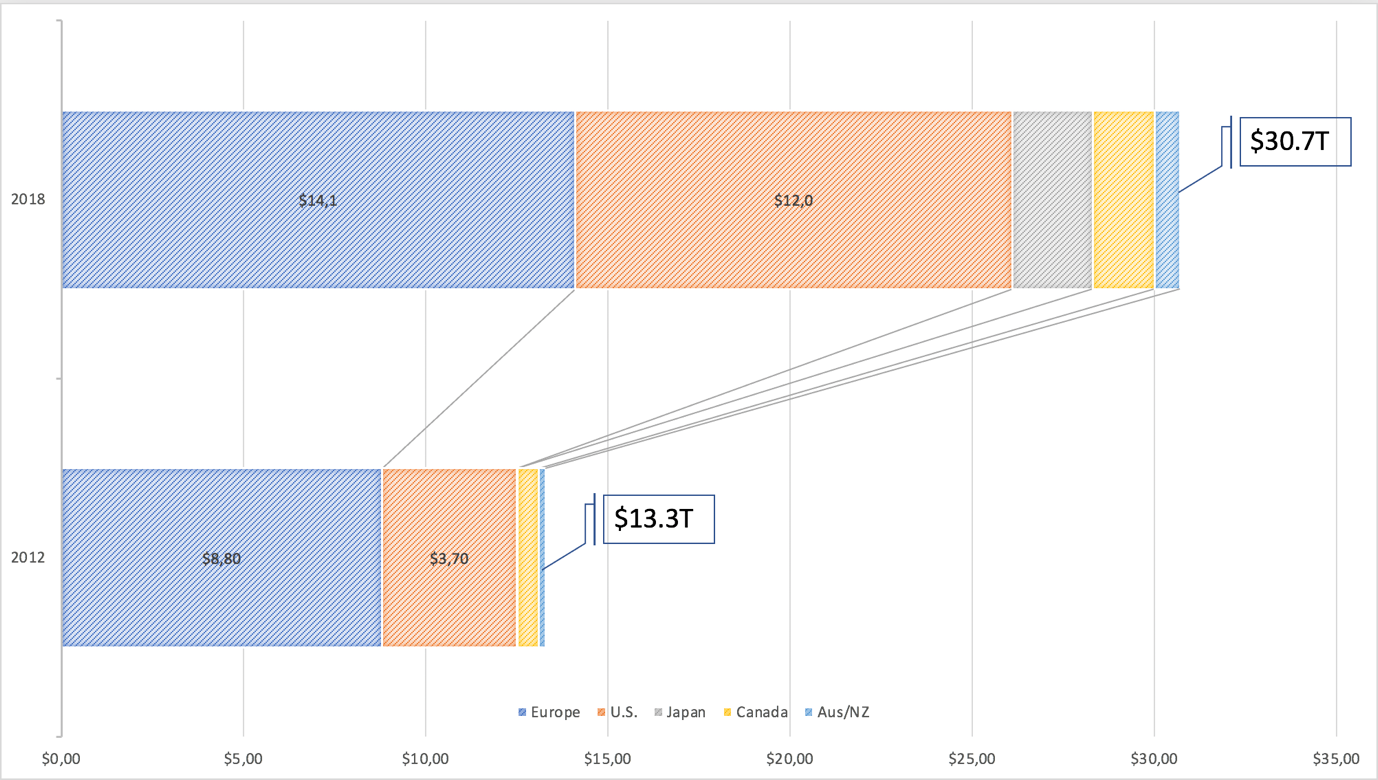

These relatively young markets have picked up steam over the last decade. In 2018, they were worth more than 30 trillion dollars, with the potential of hitting 53 trillion dollars by 2025. Today, Europe leads with 14 trillion dollars; the American market, having grown roughly 30% since 2012, trails at 12 trillion dollars (Figure 1, GSI Alliance).

Figure 1: Sustainable Investment Market Size (USD Trillions)

From 2019 to 2020, according to Bloomberg reports, investment in a cost-effective basket of ethical securities known as ESG exchange-traded funds (ESG-ETFs) tripled.

The rapid growth of the ESG market has attracted many players thirsty for yields in a market with low interest rates. However, they did not necessarily end up with the product they thought they were buying.

People do tend to care about what happens to their savings and whether their money is ethically spent. Many have ethical concerns as to whether their money does harm in the world or whether it is a force for improving planetary ecosystems.

For example, in its attempts to respond to calls by investors to accelerate its green transition, Exxon Mobile has proposed a carbon capture system, which would be stored underground and could attract 100 billion dollars in investments.

Yet, in order for this to become a reality, it will require a lot of ‘public support’ (read: funding). Even then, and most importantly, the cash flow would end up in oil and gas production.

That is greenwashing.

In Europe, this has prompted MEPs and civil society to lobby the European Commission to exclude low carbon fossil fuels from the Renewable Energy Directive, setting the battle lines with the oil industry.

Perhaps unsurprisingly, regulators are slow to label this particular type of fruit juice stand a gimmick, which leaves investors perplexed and frustrated once they realise they have been drinking Kool-Aid all along.

Jars, labels and quality

Across the pond, the Security and Exchanges Commission — Uncle Sam’s financial watchdog in chief — has no standard label and often times the raters disagree about the nitty-gritty criteria.

In fact, ad-hoc ESG raters have been springing up, yet, according to research by MIT, their ratings correlate 0.61 on average, whilst credit ratings from established institutions average 0.99 on a standard 1.00 scale.

In Europe, we lack an authority with the single market powers our transatlantic cousins possess. This ommission exposes us to a less regulated and more fragmented market that puts investors at risk of buying into a marketing scheme that can trash their hopes of a sustainable future.

From a regulatory perspective, the name of the game is how much the issuers of ESG securities must tell the regulators and, in turn, how much those selling must disclose to the public. Brussels is working on establishing a Green bond standard, with clear eco-labelling for financial products and taxonomy of sustainable practices for private concerns.

This primordial market sophistication is causing some market players to feel disillusioned. The former BlackRock CIO of Sustainable Investments, Tariq Fancy, calls ESG nothing more than wishful thinking that once put into execution amounts to little more than PR spin.

In part, this is because American portfolio managers are legally bound (as well as financially incentivised) to do nothing that compromises profits. In essence, advancing real change in the environment simply does not yield the same return.

As the strategist and policy expert Michele Wucker, author of You Are What You Risk, puts it: “Many mutual funds billed as ‘sustainable’ are simply repackaged ways of investing in the usual FAANG suspects – the stocks of the five most popular and best-performing American technology companies: Facebook, Amazon, Apple, Netflix and Alphabet (Google)”.

Deceptive labels

Returning back to the ESG ETF boom, today’s regulatory environment cannot guarantee investors certainty as to what it is they are pouring their money into.

BlackRock’s iShares ESGU, iShares ESG Aware MSCI EM ETF (ESGE) and iShares ESG Aware MSCI EAFE ETF (ESGD) – which includes stakes in Exxon Mobile and Chevron Corp – account for about 13.4 billion dollars of year-to-date flows.

BlackRock’s products filter out companies involved in civilian firearms, controversial weapons, tobacco, thermal coal and oil sands, opting for a passive approach to change.

A peer fund from Vanguard Group takes a stricter approach: Its 2.2 billion dollars ESG US Stock ETF (ESGV) excludes companies involved in adult entertainment, alcohol, tobacco, weapons, fossil fuels, gambling and nuclear power.

“While all this is arguably preferable to putting your money in fossil fuels, it’s not making the kind of impact we need: getting investment to new, clean and efficient technologies, or supporting economic growth where it’s most needed”, Wucker tells Brussels Morning.

Filtering the juice

So what can European leaders do?

According to Wucker, “business leaders and policy makers need to back serious, credible standards that will make a difference instead of giving the nod to business as usual”.

“Policy makers might even consider a carrot-and-stick approach: favourable tax treatment for companies that make the most aggressive moves in reducing their own emissions and investing in clean technologies, and penalties for firms that make false green claims or generate the most unwanted side effects like greenhouse gases or abysmal treatment of workers”.

Market trailblazers, recognising the perils of greenwashing for the planet and for the market, are now beginning to take a proactive approach.

Nevertheless, market self-regulation in ensuring quality standards for consumers often does not yield the desired results, especially when dealing with complex systems such as financial markets.

In the end, only government action, through the coupling of science and policy, offers the right recipe to ensure the quality of what’s in the juice jar and assurances about the planet’s sustainability.

These views are those of the author and not the editorial team at Brussels Morning.